Insights

Data-Driven Business Transformation by Infosys

By Theodora Lau, founder of Unconventional Ventures, an advisor and a contributor to top industry events and publications.

Building the next generation of human-centered business with data

How can you build business resilience and adapt in a rapidly changing market? In a world where we are immersed in an enormous amount of data, how do we decipher the insights from the bits and bytes? What is the data telling us about people, process, and technology? And most importantly, the customers that we serve?

From sustainability to the future of work and digital transformation, data plays a key role in our everyday lives, pointing us where changes are happening and where we should optimize. Here are a few figures to consider from these three megatrends.

$120 Billion: 2021 was a record year for ESG (Environmental, Social, and Governance), with an estimated $120 billion poured into sustainable investments according to Bloomberg, more than double the $51 billion of 2020. And the trend shows no signs of slowing.

With increased awareness and push for corporate responsibility, the question is no longer whether to factor ESG metrics into decision-making, but rather, what sustainability data to use, from whom, and how to incorporate it into the investment process.

55 percent: According to a recent survey, work flexibility would be a make-or-break deal for 55% of the employees. Increasingly, employees are expecting more flexible work arrangements to accommodate their lifestyle and personal obligations and provide fulfillment and purpose. This presents an opportunity for leaders to re-imagine not only what work is and where we work, but when we work and how we work. Beyond deploying tech tools to facilitate collaboration amongst decentralized teams, how can we best retain the talent that we have and support them through their careers?

The future of work will be workplaces that are multimodal, supported by infrastructure and technologies that allow employees to connect anytime and collaborate from anywhere.

67.1 percent: According to DataReportal, 67.1% of the world’s population now uses a mobile phone, with unique users reaching 5.31 billion by the start of 2022. Global internet users have climbed to 4.95 billion at the start of 2022, or 62.5% of the world’s total population. From consuming content to making purchases online, digital consumption has been growing at a phenomenal pace. In fact, nearly 6 in 10 working-age internet users (58.4%) now buy something online every week, with that figure continuing to rise throughout 2021.

Welcome to the world that never sleeps, where every 1 minute of the day:

- 6 million people shop online

- Amazon customers spend $283k and Instacart users spend $67k

- Venmo users sends $304k

- Microsoft Teams connects 100k users

- 5.7 million searches are conducted on Google

With such a fast-growing data economy, it is no wonder that it is estimated that 463 exabytes of data will be created each day on a global basis by 2025.

How will organizations stand out and meet the changing needs of customers? Merely driving efficiency is no longer enough; the winning organizations will be those who are data-driven and are able to deliver unique value for their customers.

And it all starts with data.

What is your data strategy?

Without a doubt, data is one of the most powerful assets for any organization. But not all data is created equal, more doesn’t necessarily mean better. The data that you collect and ultimately manage must be driven by your business strategy. What are your goals and what do you need to get there?

Before you embark on your transformation journey, here are a few things to keep in mind.

Data quality and standards

As the saying goes, “Garbage in, garbage out.” Since data is a key ingredient that drives decision making, the importance of data quality and standards cannot be overstated, especially for regulated industries such as healthcare and financial services.

As part of data strategy, we need to decide what data needs to be collected and the goals: Who gets to use it and what is it being used for? How do we access it and create value from it? And most importantly, what are the common measurement approaches and benchmarks?

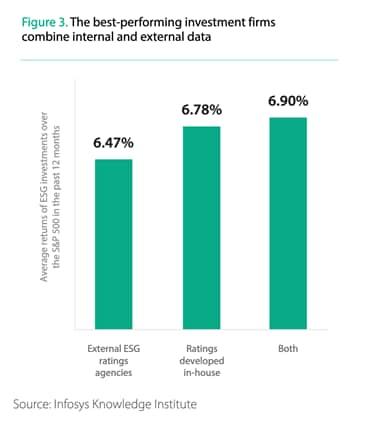

None illustrates this better than our first ESG example. According to Infosys’ recent report on the ESG data landscape, the best-performing investment firms combine internal ESG reports and external data from ratings agencies, with returns averaging 6.9 percent higher than S&P 500. Despite the advantage, however, fewer than 3% of firms surveyed are doing so.

Source: How investment firms need to navigate the ESG data landscape

Dig deeper and we will uncover further obstacles with ESG data and ratings performance: There is no single globally recognized standard in ESG reporting. And with the multitude of data providers, how best can organizations evaluate the available data sources to determine which ones(s) best meet their needs?

While ESG data will continue to grow in significance as ESG investments become more common, solving the data quality and standardization challenges is prerequisite to the essential question: What are the common end goals that we are solving for and how can we become more responsible about our true impacts?

After all, we cannot change what we cannot measure and understand.

Ethics, Transparency, and Trust

Data by itself is meaningless without insights. To be able to leverage the data, organizations need people and processes to analyze the bits and bytes, identify what is useful and what is needed, and connect the dots. As the volume of data grows and the variety of data continues to evolve, the need for a master data management strategy to allow organizations to become data rich, thereby more effectively harnessing the power of data for use in artificial intelligence (AI) and machine learning cannot be understated.

Beyond ensuring data quality, timeliness, and completeness, we also need to ensure that we have a diverse team that can help us understand the nuances within the data set. This is particularly crucial as we continue to digitally transform the enterprise, with data being the fuel powering the automation engine. While having a flawed movie or book recommendation due to biased data might not seem harmful, the consequences of introducing a flawed decision on finance (such as lending decision) or health diagnostics are far greater.

The technology, tools, and processes that monitor and maintain the trustworthiness of data and AI solutions must be rooted on ethical principles — with the purpose of leveraging the computational power of modern science to create better and more efficient solutions to benefit humankind, beyond improving operational efficiencies. As the use of AI becomes more prominent in the corporate world, we must ensure that human well-being is prioritized when we adopt and accelerate the deployment of such powerful technology, especially within the financial services industry where trust is paramount.

To ensure transparency and compliance, organizations must be able to direct and monitor their AI and validate that the outcomes of these processes are fair and working as intended. The success of AI deployment depends heavily on trust: the assurance that machines had learned enough to produce ethical and trustworthy results that could be used to guide decision making, and to create fair outcomes for customers and beyond. And with more data sitting outside of the core systems and with more actions being automated, a diligent security policy must be part of a core basis of trust.

Data governance and management

The next crucial point to consider centers around the technology layer needed to manage and protect the data across heterogeneous systems. With more data being available in unprecedented volume, including synthetic data, social media data, and alternative data, enterprises must evolve their tech stack and create strong data governance in order to tap into the power of the changing data ecosystem, and to safeguard against breaches and ransomware. In fact, infrastructure silos and concerns around data privacy are some of the key challenges enterprises face while managing data in hybrid or multi-cloud environments today.

Oftentimes, the need to change is also one of existentialism: According to Horizon Digital, up to 67% of customers switch brands – not due to price or features – but due to customer experience or a perceived lack of attention, personalization, and engagement by the brand.

The transformation story of Vanguard provides a great example of how an established firm can build a new platform from the ground up, and leverage emerging technologies such as AR, VR, and conversational AI, to enhance the retirement planning experience. One of the most exciting aspects of modernization is the ability to interact with systems outside of the Vanguard recordkeeping ecosystem and update in real time, thereby providing the advisor and the consumer with holistic and valuable insights to act upon.

As our financial needs become more complex over time, our relationships with different institutions, inside and outside of banking, will expand, along with our personal data ecosystems. Consumers will demand more leading-edge, personalized solutions that can allow them to act upon, anytime and anywhere. The winning businesses will be those that can anticipate and address such needs with the agility and security that we have all come to expect.

Talent

Beyond digital transformation driven by business needs and consumer demands, as a society, we are grappling with megatrends that transcend geographical boundaries, from aging society and rising inequality, to changing nature of work and climate crisis. Tackling the challenges in front of us will require us to rethink every aspect of how we run businesses and our roles in society.

According to IDC’s Worldwide IT Industry 2020 Predictions report, “enterprises across the global economy will need to create some 500 million new digital solutions by 2023 — more than the total number created over the past 40 years.” Beyond platforms and tools, organizations will need the right people and processes to promote true transformation, make data-driven decisions, and build a culture of data-driven innovation — with human centricity at the heart of it.

“Being human-centric means that empathy, accountability, and trust are the cornerstones of technological developments. If nudging people to buy a new health product or take out a life insurance policy is based on behavioral breadcrumbs we leave behind, then we who use these systems should be richly aware of what those breadcrumbs are.” ~ Nandan Nilekani. Chairman, Infosys

Companies that apply purpose to translate strategy through technology will also create benefits for the bottom line, planet, and people as well, according to Mohit Joshi, President of Infosys. Ikea is a great example that demonstrates that purpose and profits can, and do, co-exist. In its three-year transformation, IKEA’s share of revenue from e-commerce has jumped from 7% to 31%; and the company produced strong profit growth of 24%, despite just a 1% increase in revenue.

As cited in the Infosys Digital Radar 2022 Report, ESG commitment significantly impacts an organization’s transformation effectiveness, which can in turn add $357 billion in profits globally amongst the companies surveyed.

Transformation for tomorrow

In a world that is hyper focused on possibilities, we must remember that beyond improving the bottom line, we also have responsibility to each other and our society. As we continue to adopt new technologies to transform our businesses, we must develop ways to assess the new innovations for broader implications on our society, and ensure accountability, transparency, fairness, auditability, and trustworthiness. And we need to look beyond the bits and bytes of binary data and recognize the larger collective impact of our actions: our shared prosperity.

Behind each data point is a call to action. With intention, we can create a more human-centric and equitable future for all.

Request for services

Find out more about how we can help your organization navigate its next. Let us know your areas of interest so that we can serve you better.