Success Stories

Learn from our clients how we’ve been empowering them

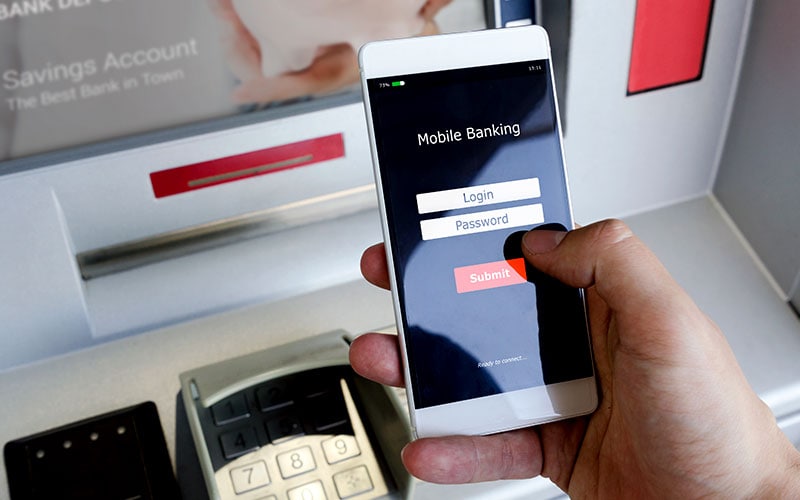

Success Story

Success Story

Rapid, significant change is happening in financial services. Customer expectations are shifting while big tech, fintech and agile new players carve up traditional value chains, blurring industry boundaries. In response, financial institutions must make digital transformation happen, faster than the speed of change.

Infosys helps financial institutions to navigate complex transformational journeys to make end-to-end transformation a reality, so they can outpace change to outperform the market.

Opinions about us from leading independent industry analysts and advisors

Learn from our clients how we’ve been empowering them

Success Story

Success Story

Explore Solutions